Australia’s banking regulator, the Australian Prudential Regulation Authority (APRA), has introduced new debt-to-income (DTI) lending rules that take effect from 1 February 2026. These changes are designed to promote financial stability and ensure banks lend responsibly amid rising household debt and competitive housing markets.

What Are the New APRA Debt-to-Income Rules?

Under the updated framework:

-

Banks and authorised deposit-taking institutions (ADIs) must limit high-DTI lending so that no more than 20% of new home loans have a debt-to-income ratio of six times income (6×) or higher.

-

This cap applies separately to owner-occupier and investor lending, meaning each category gets its own 20% allowance.

-

High-DTI loans aren’t banned—they just become more limited and competitive within each bank’s lending quota.

A debt-to-income ratio compares how much someone wants to borrow relative to their gross annual income. For example, a borrower with a $100,000 income seeking $600,000 in debt has a 6× DTI ratio.

Why Has APRA Introduced These Rules?

APRA’s rationale is centred on macroprudential risk management:

-

Household debt levels have climbed, and property prices in many parts of Australia remain high.

-

Easier lending conditions and reduced interest rates can encourage borrowers to stretch their borrowing capacity, potentially increasing financial vulnerabilities.

-

By capping the share of high-DTI loans, APRA aims to contain systemic risks before they escalate, strengthening banking sector resilience.

These changes are pro-active rather than reactive—aimed at mitigating future risk rather than responding to existing lender distress.

How the Changes Affect Home Buyers

For first home buyers and owner-occupiers, the short-term impact is likely to be modest:

-

Most first-time buyers borrow well below the 6× DTI threshold under current interest rate conditions, so many will not be directly impacted.

-

However, for higher-income buyers with large loan requirements, the rule could mean more scrutiny and competition for high-DTI lending spots at banks.

-

Borrowers may need to engage early and compare lenders, as some banks may reach their 20% high-DTI cap faster than others.

Effects on Property Investors

Investors are more likely to feel the impact sooner because:

-

Investment loans often have high DTIs due to tax strategies like negative gearing and interest deductibility, which can inflate borrowing relative to assessable income.

-

Banks with a high share of investor lending may hit their high-DTI cap quickly, making it harder for investors to secure loans above 6× income until quotas reset.

-

Some investors may explore non-bank lenders or specialist finance options not subject to the same cap to get the borrowing flexibility they need.

What This Means for the Property Market

Borrowing behaviour:

The rule doesn’t reduce the overall amount people can borrow under standard serviceability tests, but it does change which loans get approved first and how banks allocate their lending capacity.

Market demand:

Where high-DTI loans would have been more common, tighter quotas might cool some of the most aggressive borrowing activity. For investor demand in particular, this could slow down rapid portfolio expansions.

Price implications:

Experts suggest the DTI cap alone isn’t likely to cause a sharp downturn in prices, but in combination with other economic factors (like interest rates or broader lending conditions), it could influence buyer behaviour and sentiment.

Preparing for the New Rules

If you’re planning to buy or invest:

-

Review your DTI ratio: Understand where you stand relative to the 6× threshold.

-

Shop around lenders: Different lenders will manage their high-DTI allocations differently.

-

Consider alternative strategies: Joint applications, larger deposits, or structuring across lenders can lower your individual DTI and improve approval chances.

Final Thoughts

APRA’s new debt-to-income limits mark a significant shift in Australian mortgage regulation. They aren’t designed to restrict access to credit for the majority, but rather to manage systemic risk and create more stable lending practices across the banking system.

For buyers and sellers, staying informed about these changes can help you navigate the market more effectively—especially in high-growth conditions where borrowing limits and lending behaviour will increasingly shape opportunities in the property sector.

You might also be interested in

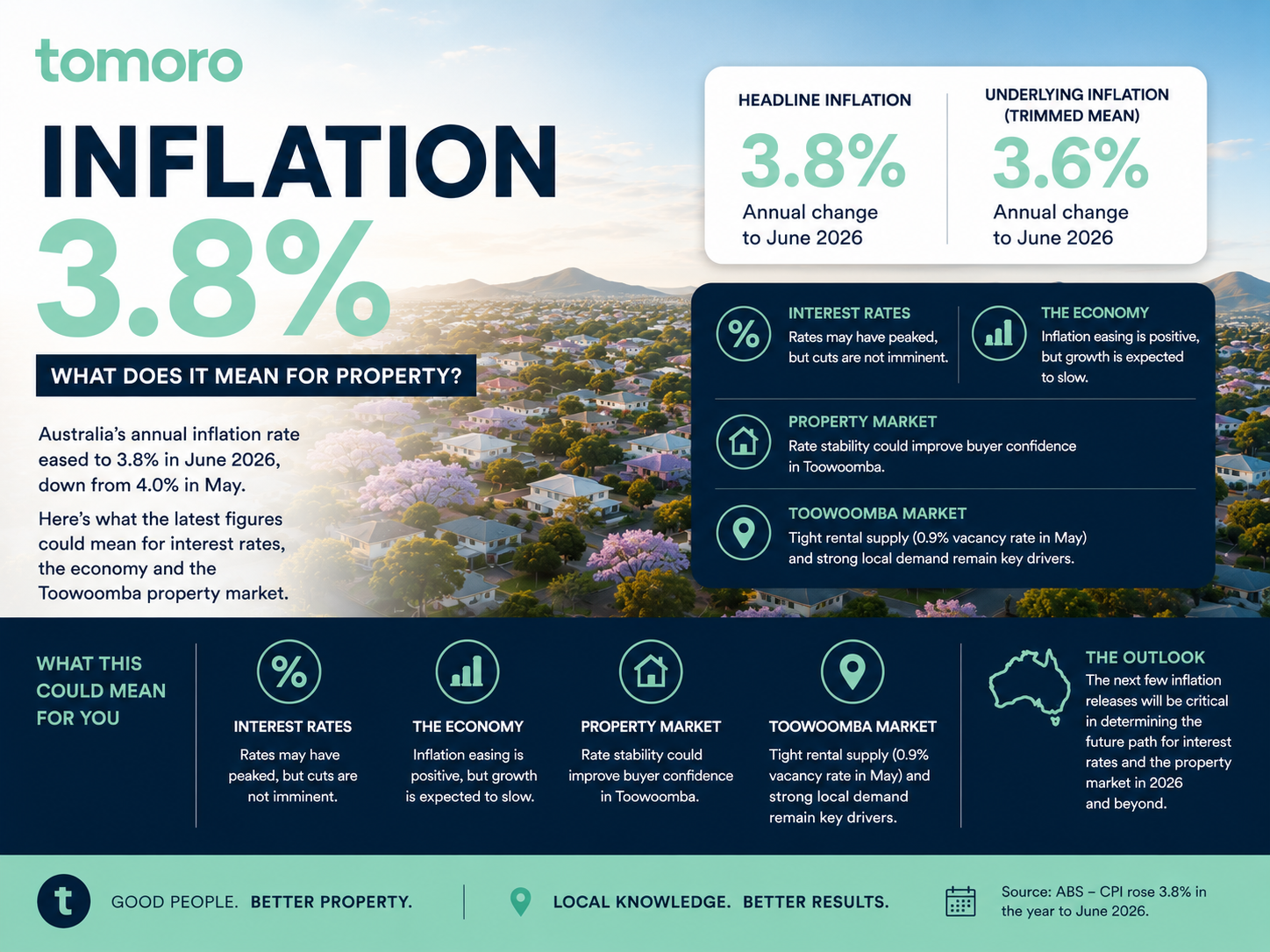

Jul 29, 2026

What Could It Mean for Interest Rates and Toowoomba Property? Australia’s latest inflation figures have delivered some encouraging news for households, borrowers and the property market, with annual i

Jul 19, 2026

Everywhere you look, property investing is marketed as the path to becoming wealthy. Social media is filled with stories of investors building portfolios of ten properties before they're 35. Headlines