What It Means for Mortgage Repayments and Borrowing Capacity

Australia’s interest rate cycle has shifted again in 2026, with the Reserve Bank of Australia (RBA) resuming rate hikes in response to persistent inflation pressures. For homeowners, buyers, and investors, this change has immediate and measurable impacts—particularly on repayments and borrowing capacity.

Latest Interest Rate Increase in Australia

In March 2026, the RBA increased the cash rate by 0.25% to 4.10%, following an earlier rise in February.

This move reflects ongoing concerns around inflation, which remains above the RBA’s target range, driven by strong economic activity and global factors such as energy price shocks.

For borrowers, even a modest 0.25% increase can have a significant impact on monthly repayments and long-term affordability.

Impact on a $700,000 Mortgage

Using current market estimates and recent lender data, a 0.25% rate increase typically adds:

-

Around $100–$120 per month on a $700,000 mortgage

-

Approximately $1,200–$1,440 per year

This aligns with broader market data showing:

-

~$118/month increase on an average $736,000 loan

-

~$91/month increase on a $600,000 loan

Estimated Repayment Change (Example)

| Loan Size | Rate Increase | Monthly Impact | Annual Impact |

|---|---|---|---|

| $700,000 | +0.25% | ~$110 | ~$1,320 |

Key takeaway:

While the increase may seem small, repeated hikes compound quickly—placing real pressure on household cash flow.

How Interest Rates Reduce Borrowing Capacity

Interest rate increases don’t just affect repayments—they also reduce how much buyers can borrow.

As rates rise, lenders:

-

Increase assessment buffers

-

Reduce maximum loan sizes

-

Tighten serviceability calculations

Typical Borrowing Capacity Impact

A 0.25% rate increase generally reduces borrowing capacity by ~2.5% to 3%.

Borrowing Capacity Comparison

| Previous Borrowing Capacity | Reduction (approx.) | New Borrowing Capacity |

|---|---|---|

| $500,000 | -$12,500 to -$15,000 | ~$485,000 |

| $700,000 | -$17,500 to -$21,000 | ~$679,000 |

| $1,000,000 | -$25,000 to -$30,000 | ~$970,000 |

Important insight:

This reduction compounds with each rate rise. Multiple increases in 2026 could significantly shrink buyer budgets.

Flow-On Effects for Buyers and Sellers

Buyers

-

Reduced borrowing power limits purchasing options

-

Increased repayments impact affordability

-

Greater caution in decision-making

Sellers

-

Smaller buyer pools at higher price points

-

Potential softening in price growth

-

Increased importance of strategic pricing

Investors

-

Higher holding costs

-

Yield becomes more critical

-

Greater focus on cash flow-positive assets

What to Expect Moving Forward

Forecasts suggest further rate increases remain possible in 2026, with major banks anticipating additional tightening if inflation persists.

This means:

-

Borrowing capacity may continue to decline

-

Mortgage stress could rise

-

Property market growth may moderate

Final Thoughts

Interest rate increases are a powerful lever in the property market. While they are designed to control inflation, they directly impact borrowing capacity, affordability, and buyer behaviour.

For property owners and buyers, the key is not just reacting—but planning:

-

Reviewing loan structures

-

Stress-testing repayments

-

Understanding borrowing limits before making decisions

In a rising rate environment, informed decisions become the difference between opportunity and risk.

You might also be interested in

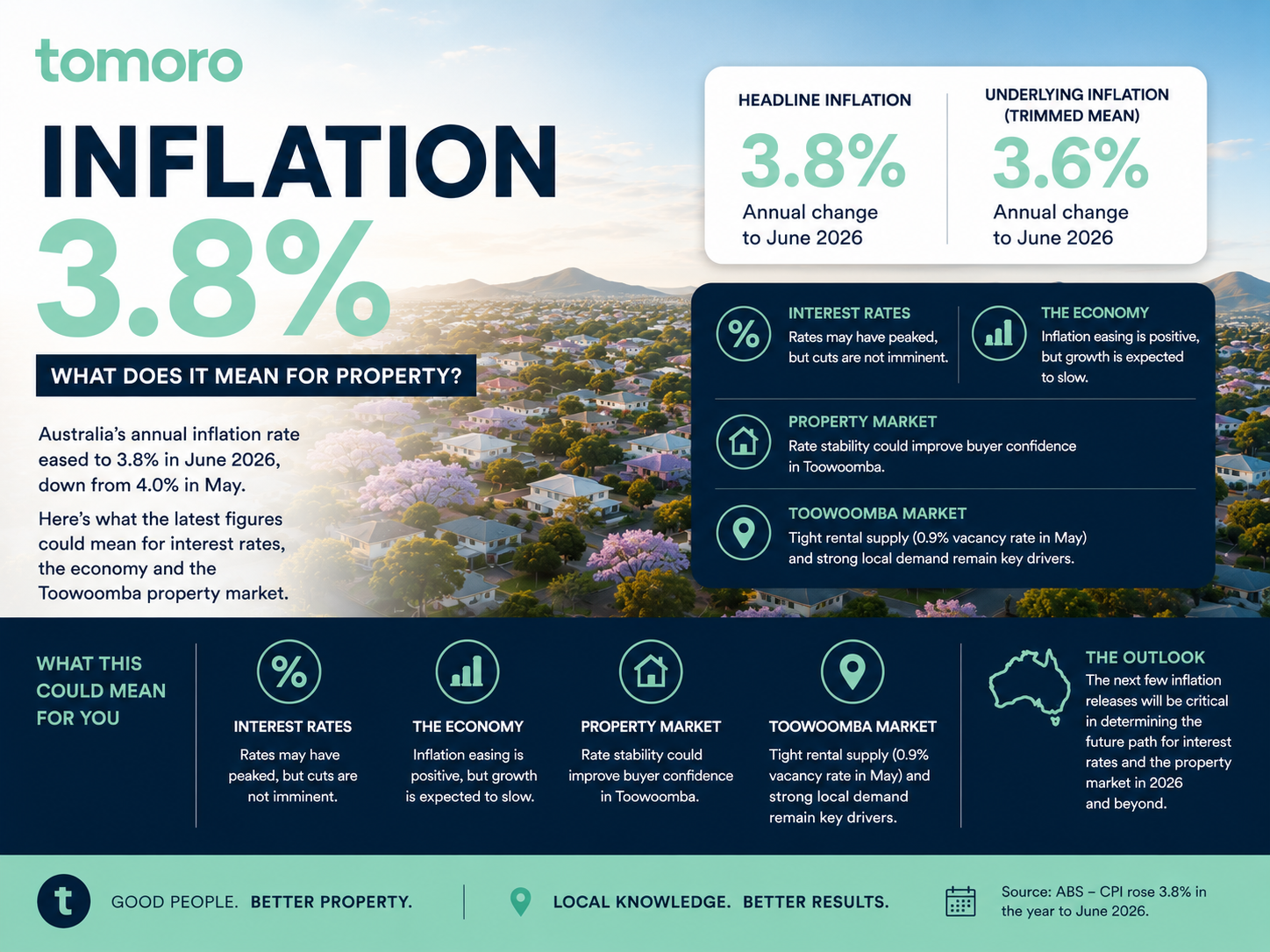

Jul 29, 2026

What Could It Mean for Interest Rates and Toowoomba Property? Australia’s latest inflation figures have delivered some encouraging news for households, borrowers and the property market, with annual i

Jul 19, 2026

Everywhere you look, property investing is marketed as the path to becoming wealthy. Social media is filled with stories of investors building portfolios of ten properties before they're 35. Headlines