Before you start scrolling through property listings, there are a lot of things you need to prepare yourself for, most of which are financial. Buying a house for the first time or the tenth time can be equally financially challenging, and if you don’t have the correct information, it can get overwhelming and complicated very quickly.

It's recommended to discuss your decision with property investors beforehand, so they can advise you on how much you have to save up for the kind of property you want. Real estate agents also provide tips for property investors to help them make the right decisions.

The housing market is highly competitive, with listing prices climbing up to 13.5% since December 2021. If you are a first-time property investor in Australia, you need all the help you can get to know the logistical groundwork, the finances involved, and the hidden costs, so you are prepared and have adequate funds saved up when you buy your first property.

This article will discuss smart property investment tips, so let’s get started!

1. Set Your Down Payment

The median house price in Toowoomba and Queensland, rose to $530,000. Thus, the first thing you need to do after choosing to buy a property is save up funds for the down payment. Typically, the down payment can range from 3.5% to 20%. Thus, you won’t necessarily have to save up a lot of money before buying your dream house, but it is considered beneficial to pay more money upfront.

Down payment affects the balance you owe; the more you save up, the less risky you would be to lenders. The larger down payment means less in the way of monthly payments and mortgage.

It’s best to partner with a trusted professional and go over the loan options, and down payment assistance programs available through government schemes. With these assistance programs, you can qualify for a mortgage and save yourself from Lenders Mortgage Insurance (PMI).

Be a smart Toowoomba property investor and save up on a down payment with the following tips:

- Develop a budget and timeline.

- Automate your savings and deposit a percentage of your salary to a dedicated savings account.

- Monitor your expenses and try to reduce your monthly spending.

- Increase your income or save through a side hustle.

- Look into home-buying programs and consider all housing options before deciding.

2. Plan For Contract Deposit

Another thing you need to consider when buying a property is the contract deposit. This is a deposit made to the seller to show a buyer’s good faith when buying a home. The deposit is considered a part of the initial down payment and helps you save time for extra financing and inspection before closing the deal.

With such a highly competitive housing market and multiple Australian property investors, it becomes increasingly difficult to stand out and close the deal on your dream house. The deposit can be anywhere from 1 to 10% of the sale price and varies on the market research, the seller, and the real estate agent you are working with.

Generally, this is deposited with the purchase agreement or sales contract but can also be attached to the initial offer. This shows the buyer is serious about the property, and once the seller chooses you, you get extra time to inspect the property and leave the house if you notice any problems later.

3. Know Your Borrowing Limit

If you can’t save enough funds for a down payment and risk losing out on your dream property, you can always take a loan. Your borrowing limit depends on your income, credit history, assets, and expenses. Thus, you need to work with mortgage lenders and analyse the maximum amount you can borrow. Remember one thing, though; the higher the loan, the more the ongoing mortgage repayments. Add the monthly expenses of owning a home, such as utility bills, groceries, transport, etc., and you might have nothing left for non-essential purchases.

Thus, even if your loan limit is high, it doesn’t mean you need to utilise the complete amount. Ask yourself the following questions before opting for a mortgage loan:

- Is your job secure?

- Can you handle a 2% interest rate increase?

- Do you have adequate savings to make monthly mortgage payments if you lose your job?

If the answer to all this is yes, go for a loan and make smart property investment decisions.

4. Choosing A Mortgage Lender

Property investors look for multiple things when choosing a house to buy, such as crime rate, repairs, and renovations needed, proximity to schools and local shops, etc. You need to be just as vigilant when choosing a mortgage lender.

Mortgage rates, interests, and fees are constantly changing, along with the state laws and requirements; thus, your money lender should be up-to-date, experienced, and loyal. A mortgage lender can help you evaluate your loan options and how best to proceed with the income you have.

Ask your chosen mortgage leaders the following questions:

- What type of home loans do you offer?

- What are your costs?

- What’s your procedure and timeline?

5. Get Home Loan Preliminary-Approval

Once you have determined how much you can borrow and your down payment percentage, it's time to get your home loan approved. Preapproval is an essential part of the home buying process. You can compare multiple potential mortgage lenders and discuss quotes. Moreover, obtaining a preapproval letter helps you discuss different loaning options.

A mortgage preapproval is a physical exam for your finances. It analyses key factors like income, employment history, credit score, debt-to-income ratio, credit history, and the loan-to-value ratio.

A preapproval mortgage letter is viable for 60 to 90 days and has an expiration date, so it's best not to use an outdated letter, as it can make you seem suspicious. Mortgage preapproval shows sellers that you are a serious buyer and moves you closer to home ownership.

6. Calculate Monthly Repayments

Another tip for a property investors is to calculate monthly repayments. There are a lot more costs involved than just the mortgage repayments, such as maintenance fees, property taxes, homeowners insurance, etc.; if your income is insufficient to handle them all, you might be in trouble.

For instance, property taxes can be around $3,000 to $4,000 per year, depending on the local government. Also, your home is a valuable asset and needs to be well maintained. You need to save at least 1% of your home’s value per year for upkeep and repairs.

Moreover, some mortgage lenders want to see two months of reserves before approving your loan. Even if it's not a requirement, having an adequate amount in savings is a good backup plan in desperate times. Mortgage lenders also need home insurance of around $800 to $1,500 per year to protect the property from various disasters.

7. Understand The Hidden Costs

Multiple hidden costs are associated with the home-buying process. You need to understand these to ensure adequate funds are available, as these costs are unavoidable. Let’s take a look at some common hidden costs.

● Pre-Purchase Inspections

Australian property investors should invest in pre-purchase inspections to avoid buying the wrong property. Generally, pre-inspection can cost around $500 to $600. The costs can vary depending on the area, the kind of property, and the inspector. An inspector inspects the visual areas of a property, such as the walls, floors, ceilings, roof, foundation structure, etc. The final detailed report will show you an overview of the repairs, fixes, and renovations required and help you make up your mind and start saving money.

● Agent Cost

Working with a real estate agent will help you find the best property according to your budget and requirements. The are no cost options and also the option to employ a buyers agent which can cost between 1.5-3% of the purchase price.

● Legal Fees

The legal fees and the closing costs consist of charges of various people involved in your transactions. This can include insurance, prepaid items, title examination, etc. Generally, you need a solicitor to carry out the legal work required to buy a home. The legal fees are typically around $1200 to $2000 and can vary from solicitor to solicitor; for instance, some charge a flat fee while others charge by the hour.

● Stamp Duty

Stamp duty is charged by the state government in Australia and is related to the transfer of land or property. Charges can vary depending on the security purchase or if you are a first-time homeowner. Typically, it's around 3 to 4% of a property’s value, however concessions apply to first home buyers and home owners.

● Renovations

While it might be challenging to get an estimate on renovations, through a professional inspector, you can quickly list down potential fixes and compare rates with multiple vendors. With rising inflation, saving up more than you think is necessary is best. Renovation costs also vary depending on the age of the home. Old homes have older technology, and repair costs are thrice more than average.

Once you have done your groundwork and managed your finances, you are ready to become a smart property investor. It’s recommended to work with real estate agents as they know the laws and regulations and various costs involved. Reach out to Tomoro; they specialise in selling and buying properties. They are the best real estate agents and property managers in Toowoomba and help you find the right home according to your budget and requirements.

07 4580 0811

353 Ruthven Street

Toowoomba QLD 4350

You might also be interested in

Jul 29, 2026

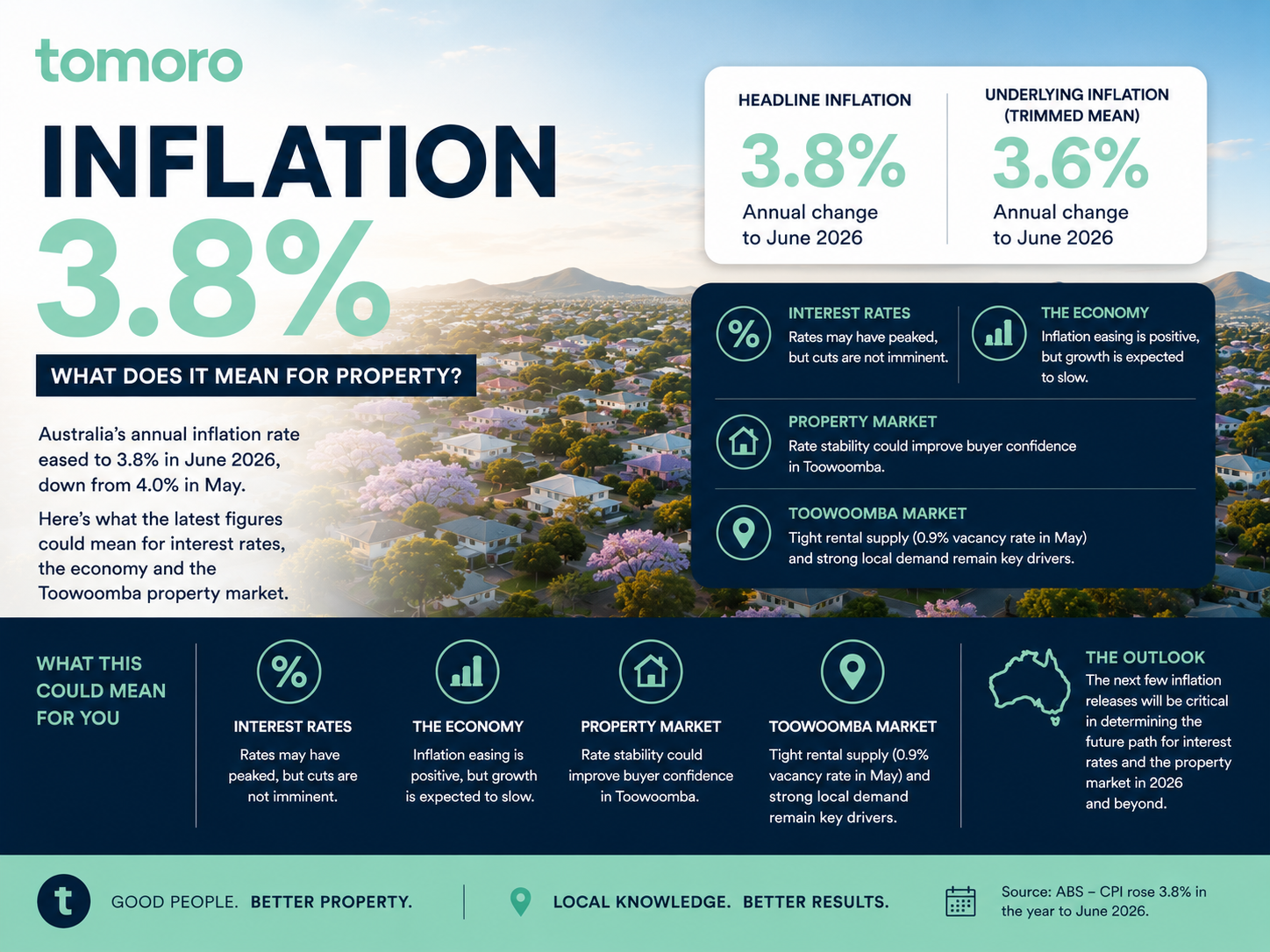

What Could It Mean for Interest Rates and Toowoomba Property? Australia’s latest inflation figures have delivered some encouraging news for households, borrowers and the property market, with annual i

Jul 19, 2026

Everywhere you look, property investing is marketed as the path to becoming wealthy. Social media is filled with stories of investors building portfolios of ten properties before they're 35. Headlines