What It Means for the Property Market

What Just Happened?

On 12 August 2025, the Reserve Bank of Australia (RBA) reduced the official cash rate by 25 basis points, bringing it down to 3.60%. This is the third reduction this year following cuts in February and May. The decision reflects easing inflation—with headline CPI at 2.1% and trimmed-mean inflation at 2.7%, both within the RBA’s 2–3% target range—and a cooling labour market, including rising unemployment.

Impact on Borrowers and Mortgage Stress

For homeowners, lower interest rates usually bring welcome relief:

-

Monthly mortgage repayments could drop significantly—borrowers with a $500,000 loan might save around $2,884 annually if lenders pass on the full rate cut.

-

Refinancing activity has surged, up about 22% in the June quarter after the May cut, as homeowners seek better rates or consolidate debt.

Property Market Reactions & Price Projections

Consumer sentiment and market activity are already responding:

-

Auction clearance rates in Sydney recently exceeded 70%, marking a 10% increase year-on-year, driven by limited stock and strong demand.

-

Forecasts suggest home price growth of around 6% in 2025, up from earlier estimates of 4%, with growth expected to moderate to 4% in 2026.

-

Econometric modelling indicates that 100 basis points of rate cuts could lift home prices by approximately 9%, with an additional cut into early 2026 potentially pushing that to 11.5%.

Property Affordability & Buyer Tensions

While borrowers benefit from lower repayments, prospective homebuyers face competitive pressures:

-

Greater borrowing capacity can increase buyer demand and bidding intensity, potentially driving prices higher—especially in markets with tight supply.

-

First-home buyers may struggle more as price growth outpaces affordability gains.

What to Watch Next

-

The RBA’s downgraded projection for productivity growth (now expected at 0.7%, down from 1%) suggests a more cautious outlook for economic expansion—a factor that could temper future rate cuts.

-

Many economists anticipate further easing, with forecasts of one more cut by the end of 2025, potentially lowering the rate to around 3.35%, and even projecting 3.10% by March 2026.

Summary Table

| Stakeholder | Key Impact |

|---|---|

| Existing Homeowners | Lower repayments, refinancing opportunities |

| Investors | Improved borrowing power, potential for higher rental yields |

| First-Home Buyers | Stronger competition, affordability challenges |

| Property Market | Rising activity and property values, especially in capital cities |

Takeaway:

The RBA’s August rate cut brings short-term relief to homeowners and supports property market activity. However, as affordability pressure mounts, especially for first-timers, the broader benefits will depend on how supply, wages, and future monetary decisions evolve.

You might also be interested in

Jul 29, 2026

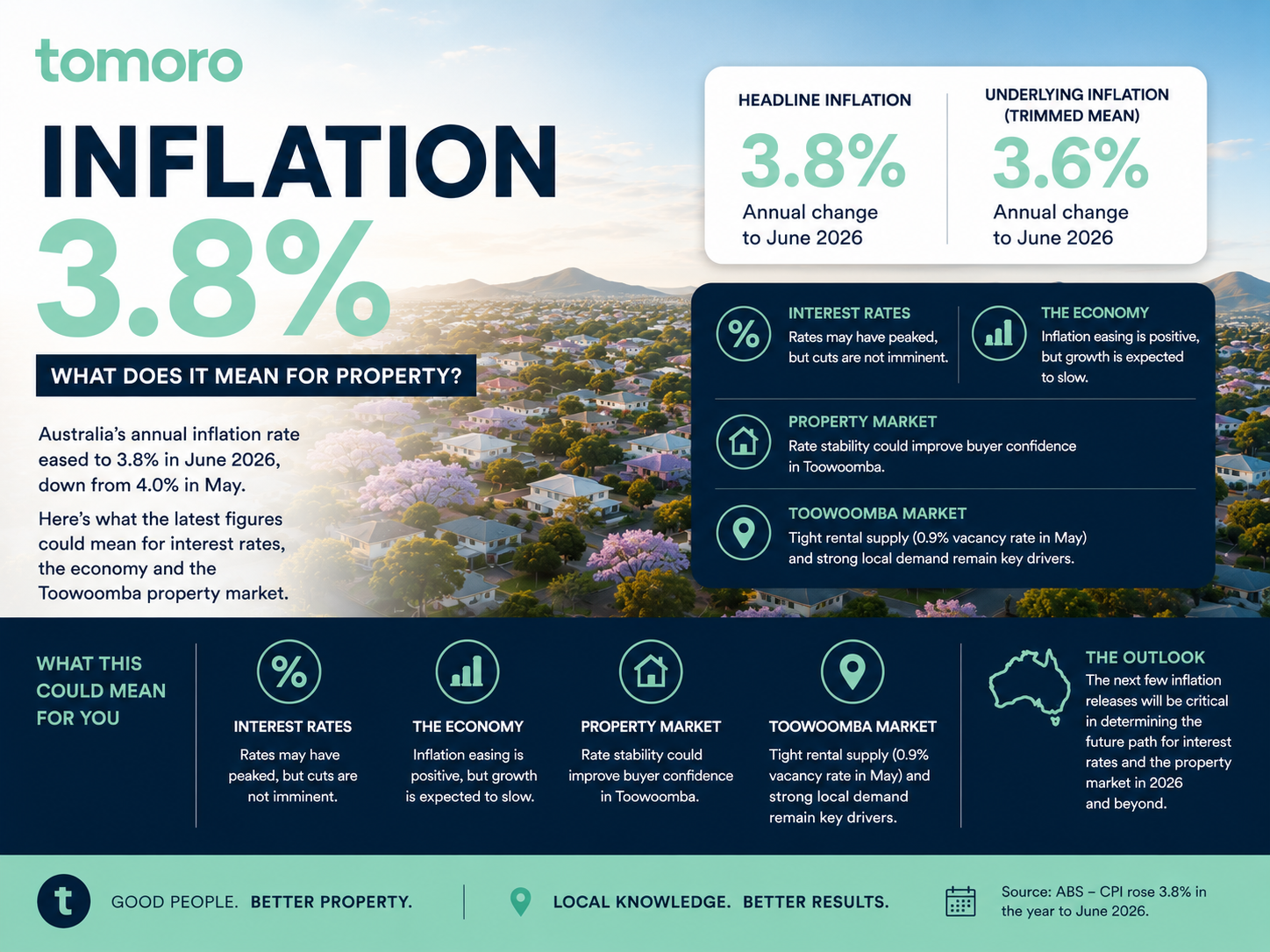

What Could It Mean for Interest Rates and Toowoomba Property? Australia’s latest inflation figures have delivered some encouraging news for households, borrowers and the property market, with annual i

Jul 19, 2026

Everywhere you look, property investing is marketed as the path to becoming wealthy. Social media is filled with stories of investors building portfolios of ten properties before they're 35. Headlines