A New Pathway to Ownership

What is the Scheme?

The First Home Guarantee—formerly known as the First Home Loan Deposit Scheme—is part of the Australian Government’s broader Home Guarantee Scheme. It helps eligible first-home buyers enter the property market with as little as a 5% deposit, eliminating the need for costly Lenders' Mortgage Insurance (LMI). The government guarantees up to 15% of the property value to the lender, enabling loans covering up to 95% of the purchase price.

Eligibility Criteria

Buyers must typically:

-

Be Australian citizens or permanent residents aged 18 or older.

-

Be first-home buyers or have not owned property in Australia in the prior 10 years.

-

Save at least 5% but less than 20% of the property value.

-

Meet income thresholds (previously around $125,000 for individuals, $200,000 for couples).

-

Purchase property under regional price caps and via a participating lender.

Recently Expanded—From 1 October 2025

Significant enhancements are launching on 1 October 2025, moving earlier than initially planned:

-

No income caps—all first-home buyers are now eligible.

-

Unlimited places—no cap on participant numbers.

-

Higher property-price thresholds, e.g., up to $1.5 million in Sydney, $950,000 in Melbourne, $1 million in Brisbane.

This expansion makes the scheme broadly accessible across the country, not just to lower-income earners.

Impact on Buyers, Sellers, and the Property Market

Pros for First-Home Buyers

-

Faster access to homeownership

Skipping the 20% deposit hurdle and LMI means many buyers can buy sooner—reducing years of saving. -

Substantial financial savings

On a $1M property, a 5% deposit avoids potentially tens of thousands in LMI. -

Expanded eligibility means more inclusion

No income limit and increased price caps bring more aspiring buyers into the fold.

Risks & Caveats for Buyers

-

Higher debt, long-term financial strain

A 95% loan increases interest paid over time and exposes buyers to higher repayment stress and risk of negative equity if property values fall. -

Limited lender options & potential for higher rates

Only participating lenders offer the scheme, potentially reducing competition and access to better rates.

Effects on Property Prices & Sellers

-

Surge in buyer demand could push prices up

Injecting more demand without a matching supply increase could inflate prices. Some experts warn of significant increases in already competitive markets. -

A windfall for sellers

More competition among buyers may benefit sellers, especially in desirable areas, making them stronger in negotiations.

Broader Market Dynamics

-

Supply remains the core issue

Without addressing housing supply constraints—through building more homes or easing zoning—rising demand may only worsen affordability. -

Taxpayer risk increases

With more guarantees in place and no income caps, the potential liability becomes a major concern if defaults rise or property prices drop.

Summary Snapshot: Who Benefits and Who Bears the Cost?

| Stakeholder | Benefits | Risks/Concerns |

|---|---|---|

| First-Home Buyers | Lower deposit barriers, avoid LMI, faster ownership | Higher debt, repayment stress, limited lender choice |

| Sellers | Increased competition may push prices higher | Could make markets overheated or unsustainable long-term |

| Property Market | Stimulates activity, supports broader access | Without supply scaling, could fuel inflation and instability |

| Taxpayer/Government | Promotes ownership, supports homeownership policy | Greater financial exposure, potential cost if market weakens |

Getting Ready: What Buyers Should Do

-

Assess your true borrowing capacity—factor in interest stress and potential rate rises.

-

Seek professional advice—compare lender offerings and understand the long-term financial impact.

-

Explore supplementary schemes—combine with other assistance like Super Saver, stamp duty concessions, or state grants.

-

Watch the market closely—greater demand may trigger faster price rises in your preferred areas.

Final Thoughts

Australia’s First Home Buyer Deposit Scheme represents a transformative shift—removing traditional deposit and eligibility roadblocks—but comes with trade-offs. For eligible buyers, it offers a chance to step into homeownership sooner. But without parallel changes in housing supply and careful financial planning, the scheme may unintentionally raise home prices, strain finances, and shift risk onto taxpayers.

As this unfolds, market participants should stay informed, balance optimism with prudence, and prioritize long-term affordability alongside homeownership goals.

More informations and to apple availabe here.

You might also be interested in

Jul 29, 2026

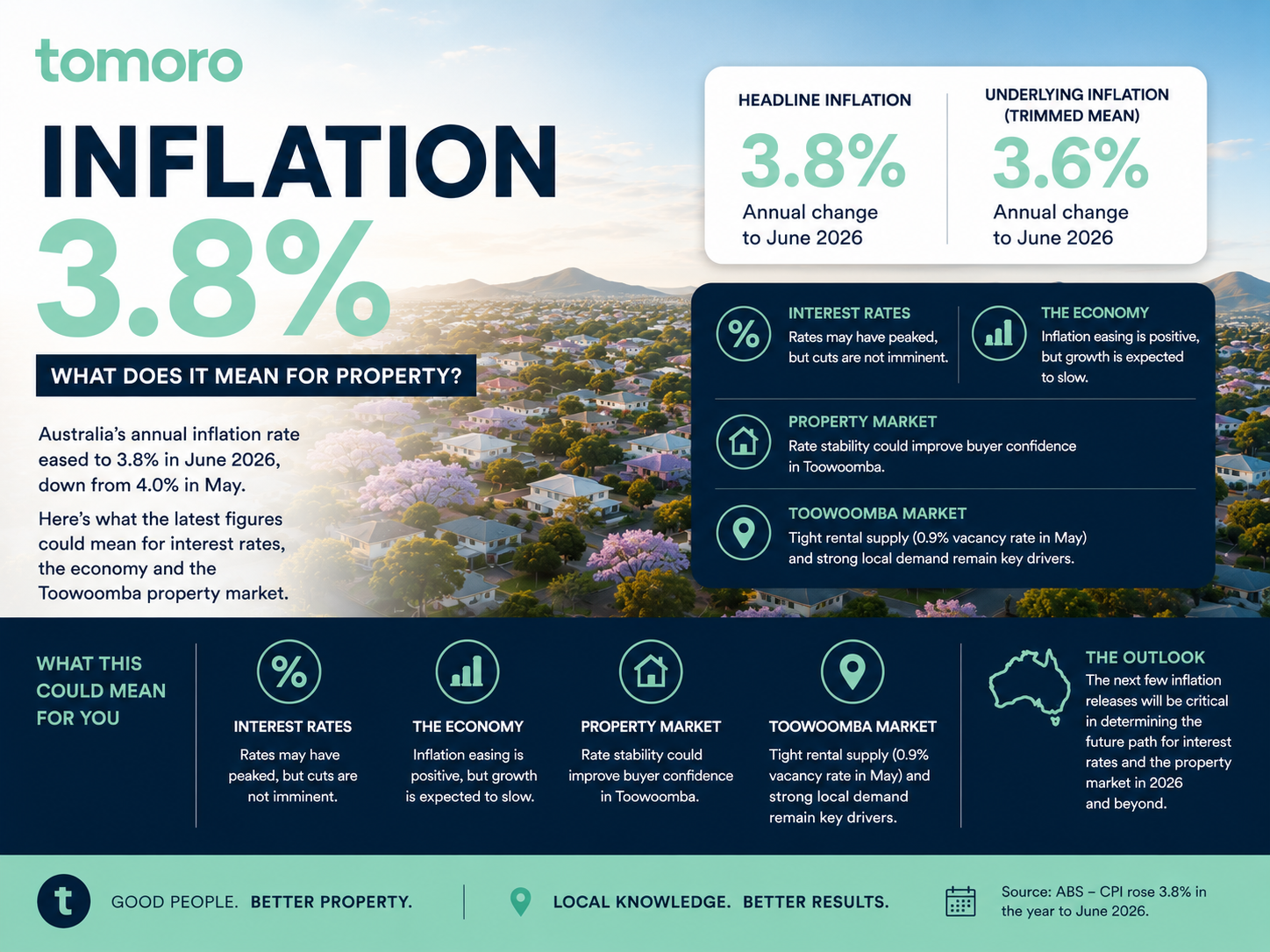

What Could It Mean for Interest Rates and Toowoomba Property? Australia’s latest inflation figures have delivered some encouraging news for households, borrowers and the property market, with annual i

Jul 19, 2026

Everywhere you look, property investing is marketed as the path to becoming wealthy. Social media is filled with stories of investors building portfolios of ten properties before they're 35. Headlines