by Tye Thies

Interest rates are a fundamental tool for regulating economic growth, inflation, and overall financial stability. In Australia, the Reserve Bank of Australia (RBA) sets the official cash rate, which significantly influences lending rates, mortgage repayments, and investment decisions. The current interest rate of 4.35%, which has been held steady, marks an important moment in Australia's economic history. In this article, we will explore the historical trends of interest rates in Australia, the factors influencing them, and how they impact homeowners, investors, and the broader economy.

Understanding Interest Rates

Interest rates represent the cost of borrowing money. When interest rates rise, borrowing becomes more expensive, discouraging spending and investment. Conversely, lower interest rates encourage borrowing, fueling growth and consumer spending. Central banks, like the RBA, adjust interest rates to manage inflation, promote economic stability, and achieve sustainable growth.

The RBA uses the official cash rate to guide the economy. By adjusting this rate, it influences short-term interest rates and, ultimately, economic activity.

Historical Trends in Interest Rates

Australia has experienced a range of interest rate cycles over the past few decades. To better understand the current rate environment, let’s look at some key historical trends in interest rates:

1980s: The 1980s saw some of the highest interest rates in Australia’s history, with rates peaking at over 17% in 1989. These high rates were part of efforts to combat double-digit inflation.

1990s: The early 1990s were characterized by an economic recession. To stimulate recovery, the RBA dramatically reduced interest rates, bringing them down to around 5-6% by the mid-1990s.

2000s: The early 2000s saw relatively stable interest rates, averaging around 5-7%. The RBA raised rates during the economic boom leading up to the Global Financial Crisis (GFC) in 2008, but rates quickly dropped following the crisis to combat recessionary pressures.

2010s: Post-GFC, Australia saw historically low interest rates. By 2016, rates had dropped to just 1.5%, a reflection of global economic conditions and efforts to stimulate growth.

2020-2023: During the COVID-19 pandemic, the RBA slashed interest rates to a record low of 0.10% in November 2020 to support the economy during the global crisis. However, by mid-2022, rates began rising as inflation surged worldwide, driven by supply chain disruptions, strong demand recovery, and other economic factors.

Current Rate Environment: 4.35%

As of September 2024, the RBA has held the official cash rate at 4.35%. This is a significant increase from the historically low rates seen during the COVID-19 pandemic but is still lower than the peaks observed in previous decades. The decision to pause rate hikes has been driven by a need to balance inflation control with the potential impact on economic growth and household spending.

Factors Influencing Interest Rates

Several factors influence the RBA’s decision to adjust interest rates, including:

- Inflation: High inflation often leads to higher interest rates as central banks aim to control price increases.

- Employment: The RBA monitors unemployment and wage growth. Higher employment levels and wage growth can lead to inflation, prompting rate hikes.

- Economic Growth: Slower economic growth may prompt the RBA to lower rates to stimulate activity, while rapid growth might encourage a rate hike to prevent overheating.

- Global Economic Conditions: Global interest rate trends, economic shocks, and trade conditions also affect Australia's interest rate decisions.

- Housing Market: Rising interest rates can dampen the housing market by increasing mortgage costs, while lower rates tend to fuel demand for property.

Impact on Homeowners and Investors

- Mortgage Holders: For homeowners with variable-rate mortgages, the current rate of 4.35% means higher monthly repayments compared to the near-zero rates seen in 2020. Those on fixed-rate mortgages may face a shock when their terms end, with significantly higher rates now in play.

- Investors: Higher interest rates can dampen demand for housing and other assets, as borrowing costs rise. However, they also provide better returns on savings and certain investment products, such as bonds.

- First-Home Buyers: Rising interest rates make it harder for first-home buyers to enter the market, as borrowing capacity is reduced. However, this can sometimes be offset by a cooling property market, leading to slower price growth or even declines.

Visualizing the Trends

Below are graphs showing the historical trends in interest rates over the past four decades and the comparison of rates during major economic events.

1. Historical Interest Rate Trends (1980 - 2024)

I’ve plotted the RBA's cash rate since 1980, highlighting key periods such as the late 1980s spike, the post-GFC reduction, and the rapid increase during 2022-2024.

2. Interest Rates vs Inflation (2000 - 2024)

This chart visualizes the relationship between interest rates and inflation, showing how rate hikes and cuts have been influenced by inflationary pressures over the past 20 years.

Conclusion

Interest rates are a powerful tool that shapes economic trends, influencing everything from mortgage repayments to consumer spending and investment decisions. The current pause at 4.35% reflects the RBA’s cautious approach, as it balances controlling inflation with supporting economic stability. As the economic landscape continues to evolve, interest rate trends will remain a key area of focus for homeowners, investors, and policymakers alike.

Stay informed on these trends, as they have far-reaching implications for the housing market and broader economy.

You might also be interested in

Jul 29, 2026

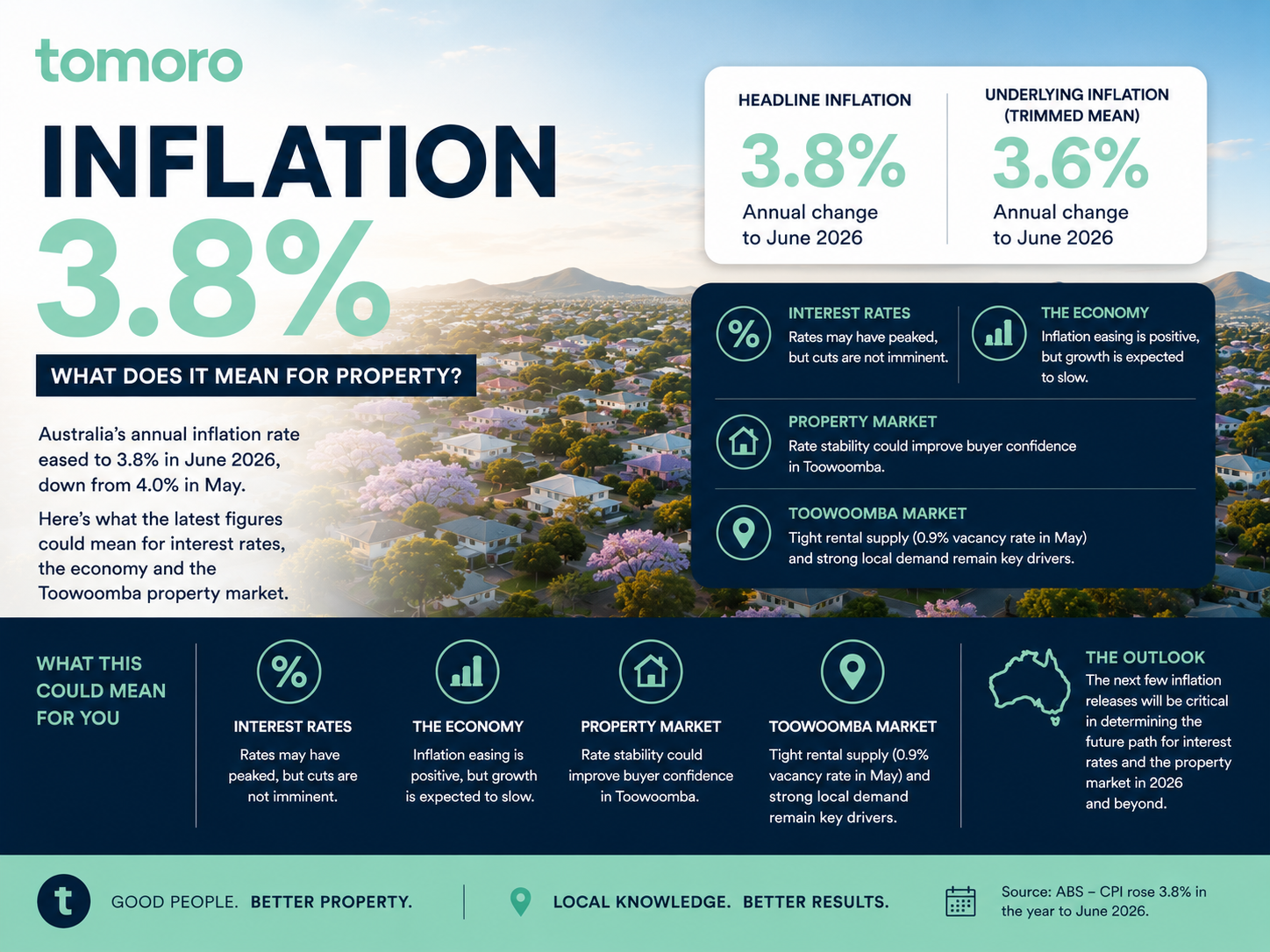

What Could It Mean for Interest Rates and Toowoomba Property? Australia’s latest inflation figures have delivered some encouraging news for households, borrowers and the property market, with annual i

Jul 19, 2026

Everywhere you look, property investing is marketed as the path to becoming wealthy. Social media is filled with stories of investors building portfolios of ten properties before they're 35. Headlines